In Q1 2026, debt outpaced equity. For a market that spent the better part of a decade idolising the VC round as the ultimate validation of a serious business, this was worth a conversation.

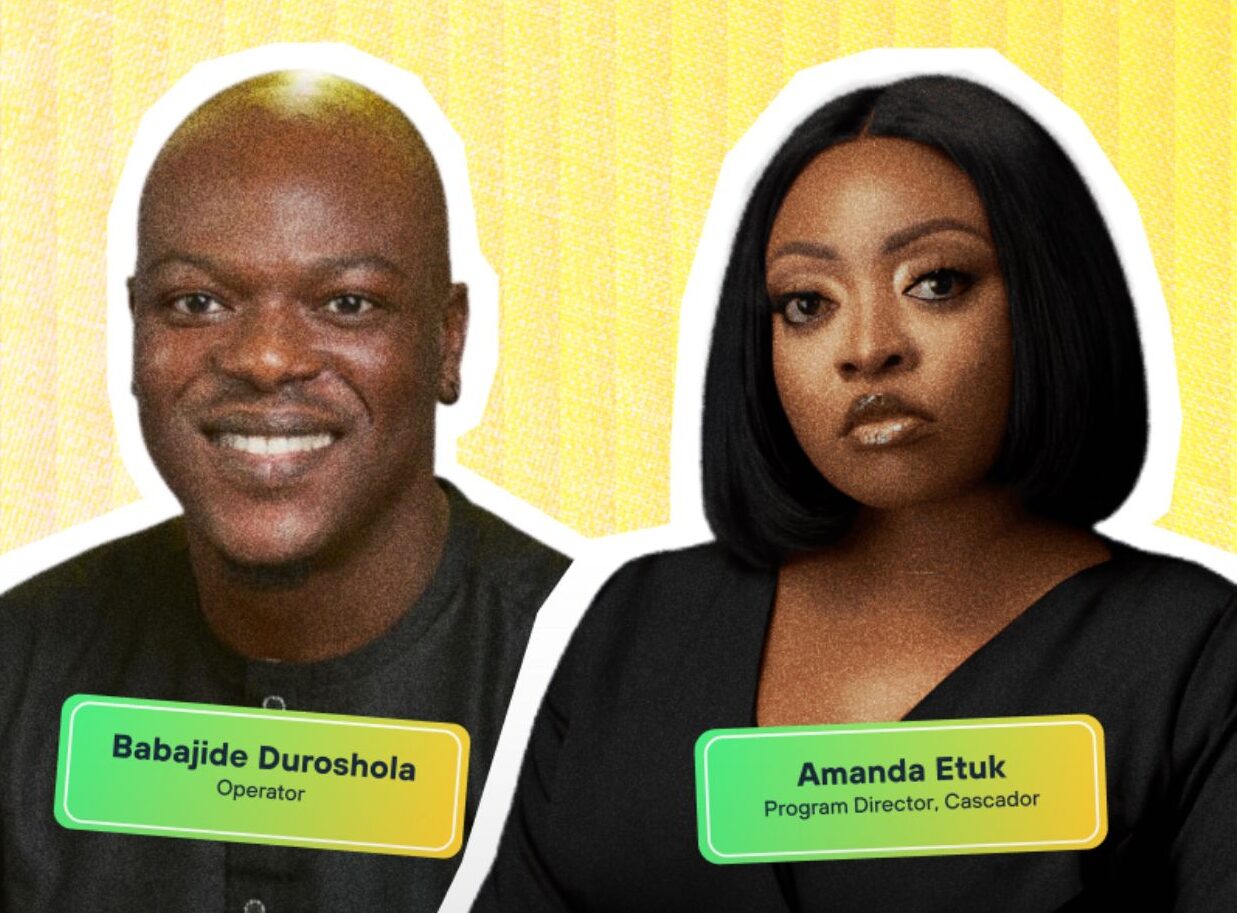

Condia hosted the Twitter Space with two guests who have seen financing from both sides of the table: Babajide Duroshola, a veteran operator with over a decade in the tech space who has personally raised close to ₦98 billion in debt facilities, and Amanda Etuk, Program Director at Cascador Africa, who, before that, spent six years co-founding Messenger NG, a logistics company in Abuja.

The era of hot money is over. That might actually be a good thing.

Duroshola opened with a blunt take about the boom years, roughly 2016 to 2022, that produced a generation of founders who confused fundraising with building. Post-Paystack exit, capital was flowing freely, and a lot of it went to ideas that had no business receiving investment.

“Thank God 2020 and 2021 are over,” he said. “People are actually properly building businesses now.”

He argues that debt capital is not a new idea. It is actually how African businesses were built before the Silicon Valley playbook arrived. You made a margin on a product, then borrowed to scale it. The trouble is that somewhere along the way, founders started building for pitch decks rather than for customers.

Etuk added that debt is not inherently better; it is just more honest about what it demands. “Debt comes with a lot of responsibilities attached to it,” she said. “You need to have established traction to even be able to say what your unit economics are.” For a business that hasn’t found its footing yet, debt is not a lifeline — it is a trap.

Read: Africa’s startups have raised over $700 million in Q1 2026. Here’s what the numbers say.

Debt is a working capital tool, not a starting pistol

Duroshola’s distinction between what equity does and what debt does provided a clear framework.

Equity is for proof of concept — building your team, testing your thesis, getting to product-market fit. Debt comes after. “Debt works in scaling existing businesses that already have product-market fit to a certain extent,” he said. “It is not there to scale an idea you are trying to test.”

The practical implication is that if you are considering debt, you need to bake the cost of servicing it directly into your pricing. If debt costs you ₦10 per unit to service, that ₦10 is included in the price of every sale. Debt only works when the unit economics can absorb it cleanly.

The kind of debt you raise also has to match your business’s rhythm. An FMCG business with fast inventory cycles might be well-served by a 365-day working capital facility — raise, produce, sell, repay, repeat. A services or infrastructure business is better served by a three- to five-year term loan that keeps capital working within the business over a longer horizon. “You need to be able to understand, based on the type of business you are running, what works,” Durushola said.

One structural challenge unique to Nigeria is that banks still think short-term. Currency volatility, political uncertainty, and macro instability have trained lenders to avoid long-term exposure. A founder walking into a Nigerian bank today is more likely to be offered 365-day working capital than a multi-year facility, not because the bank does not understand the business, but because nobody in the system is comfortable thinking five years out.

Duroshola believes this will change as more companies build strong financial records that lenders can actually underwrite.

Before you think about debt or equity, settle your fundamentals

Etuk had arguably the most pointed remarks of the evening, and they were not specifically about debt at all.

“The reason to start a business is not to fundraise,” she said. “It is to have customers and to make a profit.”

Her challenge to the founder community was that too many people with ideas are jumping straight to the question of who will fund them, instead of asking whether anyone will pay for what they are building. “The best type of capital for any business is from your customer.”

Her recommended sequencing before a founder even approaches institutional money:

First, validate the business model. Is there a real problem, and are real people willing to pay for the solution? Second, exhaust early-stage sources — friends and family, strategic angels who open doors rather than write cheques. Third, only after those options are genuinely depleted should equity or debt enter the picture.

“VC funding is not the first step,” she said. “Raising equity too early is actually a disadvantage to the founder.”

Duroshola made the same point differently, citing Paystack, Flutterwave, and Moniepoint — the founders of all three brought deep industry experience, having worked within the systems they later disrupted. The lesson being that sector knowledge, not just a sharp pitch, is what makes an idea fundable and executable.

Cascador and the case for bespoke debt

Etuk used the conversation to explain what Cascador does and the difference from what most people assume. It is not a venture capital (VC) firm, a microfinance bank, or a grant-making body. It was founded by a philanthropist committed to impact through entrepreneurship, and it only invests in alums of its own accelerator program.

The reason for that model is that by the time Cascador considers deploying capital, it already knows the business intimately. That depth allows it to design funding that actually fits the company, rather than forcing the company into a standard debt structure.

Last year, Cascador deployed ₦3 billion to a company called Drive45. Its concessionary debt rates ran as low as 22.5%. In at least One case, rather than giving a founder debt directly, the team provided a bank guarantee that allowed the founder to access a single-digit loan from Nextin Bank on a three-year term with a moratorium period. “We do not want founders to force their businesses to fit any kind of model,” Etuk said.

However, Cascador targets growth-stage businesses, not early-stage. On average, alums in the most recent cohort were generating ₦1 billion or more in annual revenue. The program is sector-agnostic, but leans toward what Etuk called “real economy businesses” — manufacturing, essential services, companies with the potential to create jobs at scale.

What to look for in a debt partner (and what to run from)

Duroshola offered a practical checklist for founders evaluating lenders beyond just the interest rate:

Watch the interest rate carefully, and model it against your cash flow cycle before you sign anything. A rate that looks manageable in isolation can become fatal when layered on top of thin margins and a slow collection cycle.

Look for lenders with a culture of refinancing. The ones willing to roll over your loan as long as you are performing, rather than pulling the facility the moment you have repaid the principal. The best debt relationships work like revolving credit: you borrow, you repay, you borrow again.

Check the collateral requirements. Is it receivables-backed? A bank guarantee? Or are they asking for your Father’s house? The type of collateral tells you a lot about the lender’s sophistication.

Moreover, be very sceptical of anything that comes too easily. “If the debt is coming too easily and they are pushing you to take the money,” Duroshola said, “you have a problem.” Credible lenders run rigorous due diligence, and that due diligence can take 12 to 18 months. Founders who bristle at that process, in Etuk’s view, are not ready for debt at all.

Etuk added a dimension that Duroshola did not mention: the lender’s personality matters. “There are organisations that even if the interest rate is, you know, from heaven. I would not advise that you take money from them.” When things go hard, as they inevitably do, you need a lender who will sit across the table and have a conversation, not One that defaults to aggression. Relationship quality is part of the due diligence, too.

One line to carry out

The conversation ended with Duroshola offering a summary: debt is for scaling already proven unit economics. If your business does not yet have proof points, do not worry about debt. Get the fundamentals right first.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: May 21, 2026