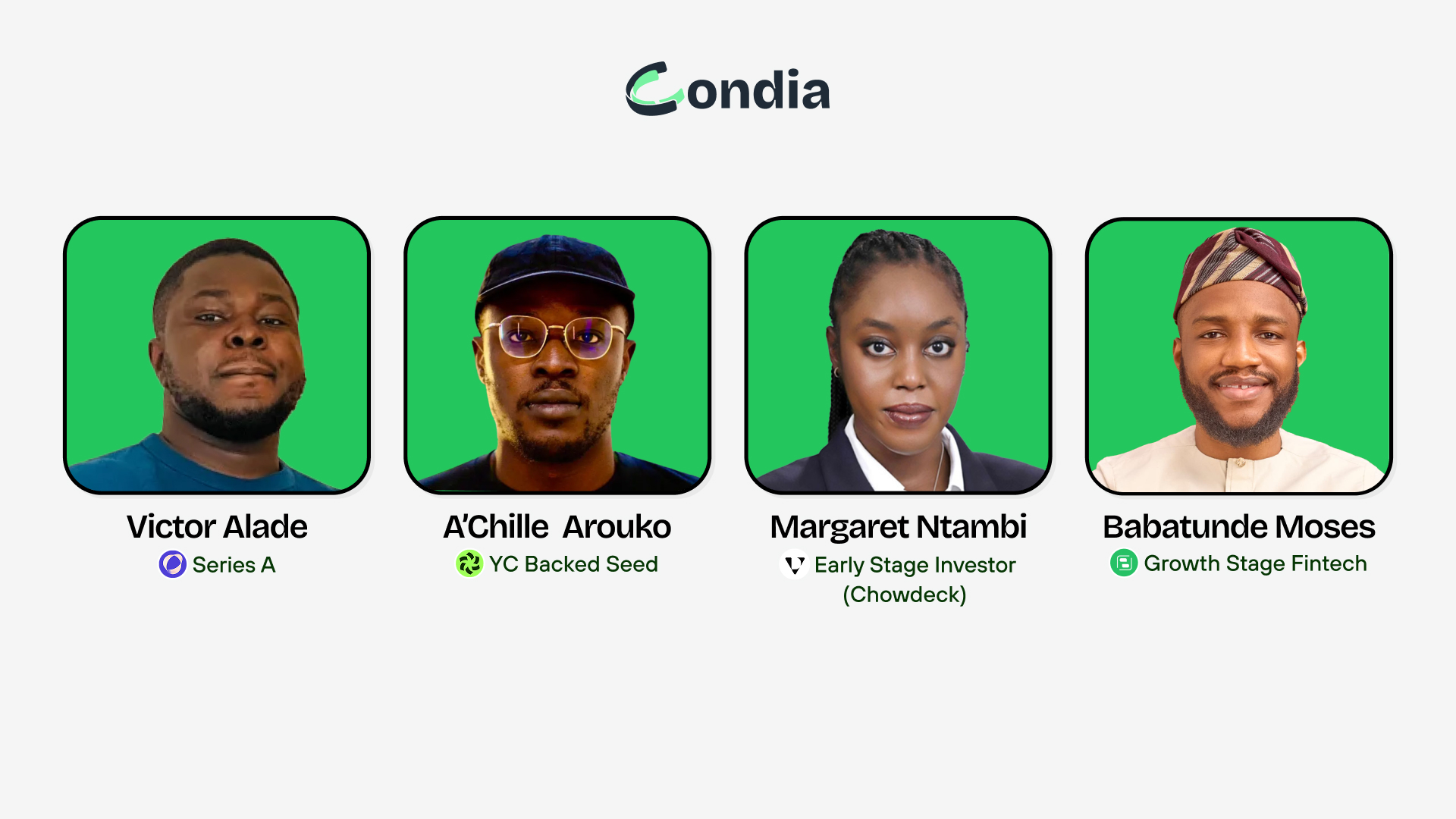

Earlier this week, Benjamin Dada, Founder of the media publication Condia, gathered four people with lived experience of Africa’s funding cycle. Victor Alade, CEO of Raenest (Series A, ’25), and A’Chille Arouko, co-founder of Bujeti, a YC W23 company. Margaret Ntambi, managing partner at Velocity Digital, an early-stage VC with 75 checks into Africa-focused companies, including Chowdeck and Terra. Then Babatunde Akin-Moses, who runs Sycamore, a credit fintech, a microfinance bank, and an asset management arm, all under one roof.

The conversation was anchored to Condia’s State of Startup Funding in Africa report and has been slightly edited for clarity.

Debt didn’t replace equity. The market has just grown up.

The first big topic was the shift in how African startups are getting capitalised. In 2025, over $1 billion flowed through non-equity instruments, and cleantech overtook fintech as the continent’s largest sector by total capital raised. For the first time, debt outpaced equity in Q1 of the year.

Margaret said this is what a maturing market looks like. The U.S. has had venture debt, bank lines, and private credit for decades. Africa has been equity-dependent by default, not by design. What’s changing is that the financing stack is finally widening. Her point is that the better question for a founder isn’t “debt or equity?” It’s what are you actually financing? If it’s product discovery and early team, take equity. If it’s inventory, receivables, or liquidity for a remittance business, debt makes sense.

Victor put numbers to it from the inside. Raenest couldn’t run a cross-border payments business without liquidity, but burning equity capital on liquidity doesn’t make sense forever. The split is now deliberate: equity for salaries and operations, debt for the float. He also made the point that raising debt isn’t as easy as people assume. The process, the scrutiny, the structure, it’s still demanding. It’s just a different kind of demanding.

Babatunde, seven years into Sycamore, is the example of what that looks like at scale. He can now raise large debt facilities that rival what an earlier-stage company would raise in equity, but that credibility took years to build. For early-stage fintechs, his honest assessment was that it’s much harder to raise equity right now, and the investors who used to deploy broadly are mostly sitting on dry powder, waiting for their existing portfolio companies to grow into follow-on rounds.

The Series A graduation problem

Ben dropped a stat from the State of Startup Funding in Africa report early on that set the tone for this: only around 10% of African startups that raised seed in 2022 made it to Series A. The median time from seed to Series A has increased from 18 months to 29 months. He’d seen the U.S. Carta data showing the same elongation and went looking for what the African version looked like. It was worse.

In 2024, African startups raised $2.01 billion across 182 deals — a 31% drop from $2.9 billion in 263 deals in 2023. And the share of funding concentrated in the top five startups kept rising: from 37% in 2022 to 40% in 2023 to 45% in 2024. The market isn’t just contracting. It’s arranging.

Margaret opined that we should stop expecting African graduation rates to match those of the U.S. The follow-on infrastructure isn’t as deep. Most Series A checks on the continent have to come from outside the continent. There are fewer deep-pocket investors at later stages, and most exits occur through secondaries and M&A rather than IPOs. The bottleneck is structure.

She added that Velocity is working to push against that through heavy diligence before they write the check, then post-investment portfolio support from an ex-operator (Ire Arikawe, co-founder of Thrive Agric) who sits with founders on milestone planning, and then scenario planning — what happens to your runway if the next 18 months go sideways? She’s also deliberately working with founders on the pre-Series A sell process, making sure they know what investors on the other side are looking for before they start the conversation.

Related Article: How to build an online community around your startup

How Victor’s Raenest actually got to Series A in the drought years

Raenest raised $11 million in its Series A, led by QED Investors, with Norrsken22, Ventures Platform, P1 Ventures, and Seedstars participating. The round brought total funding to $14.3 million, starting from a $700K pre-seed in 2022 and a $2.6M seed in 2023. What Victor described in the space was a playbook for raising in a bad market that anyone paying attention should write down.

First: he and the team accepted that the market was real. No waiting for conditions to improve. When they raised seed, they set explicit targets with their investors — here’s what we’ll do with $2 million, here are the milestones, here’s the revenue it should get us to. Then they hit those targets. When it came time for Series A, they had actual projection-versus-actual data to show. That’s the whole story, in one thread.

He also talked about keeping investor relationships warm without needing a check yet. Not blast updates, but targeted communication with people who could either lead a round or refer one. His first fundraising outreach ever was a cold DM to an angel investor on Twitter. No intro, no connection. She connected him to his first investor. He cold-messaged Ola on LinkedIn and got introduced to Oluwatobi Soyombo. Cold email and cold DMs work, but the key is selectivity — reach out to people who can actually relate to what you’re building, not everyone with the word “investor” in their bio.

The fintech fatigue is real, but it’s not the whole picture

Babatunde said it plainly: if you’re starting a fintech today, you have a lot to do to convince people. Investors who used to take those meetings are tired. The differentiation bar has moved. At the same time, growth-stage fintechs — the Moniepoints of the world are pulling enormous rounds.

He backed this up further by adding that the buzz has genuinely shifted. Cleantech, e-commerce, mobility, and the creator economy are the sectors being viewed with fresh eyes. If you’re building data infrastructure or working in a non-fintech area, you might actually be in a better position to get heard right now than you were three years ago.

Margaret gave two examples from her own portfolio of where she still sees fintech opportunity: niche plays with real product differentiation (Timon, a cross-border spending product for African travellers) and infrastructure with a clear reason to exist (Miden, which cuts card issuance integration time from 12 months to a week). If your infrastructure play can clearly show why it beats the legacy options and has a path to defensibility, people will back it. But the category alone won’t carry you.

Thoughts on exits

One of the best segments came when Ayode Akinfemiwa, a participant, asked Margaret about exits. She responded that most African startups will exit through M&A, not IPO. The earlier you understand who can buy you and why, the better your decisions get. When a founder tells her the only exit plan is an IPO, she starts to wonder if they’ve actually thought this through.

Her framing for early-stage founders: I’m coming in at a $3 million valuation. I need to know whether someone can buy you for $300 million, or whether the path to that point exists. Start having conversations with potential acquirers early, when you’re attractive but not desperate. Build something they would want.

Ben, characteristically, put a rough number on it: a good exit in Africa right now is around $25 million cash. If you’re being acquired above that, stock comes into play. That’s the ballpark to work backward from, for now.

Victor added that multiples are starting to matter again, and they’re sector-dependent. Stablecoin plays, and certain cross-border fintechs are seeing multiples above the market average. But once valuations push past $50-60 million within Africa, the pool of buyers who can write that check in cash shrinks fast. That’s a ceiling founders need to price into their strategies from the beginning, not discover at the negotiating table.

The foreigner in a foreign market question

A’Chille‘s presence on the panel also led to a thread. He’s from Benin, building Bujeti in Nigeria. When Ben asked how investors react to a foreign founder in a new market, Tunde answered that there’s scepticism (does this person have local insight?), and there’s curiosity (if they’re leaving their home market to come here, what are they seeing that I’m not?). Somewhere between those two reactions is the right call.

Related Article: How African startups can deal with the current Japa wave

A’Chille’s take was more personal: you can’t pretend the timelines are the same as the U.S. or Europe. You have to tell your investors the truth about what it actually means to build in Nigeria or Côte d’Ivoire. His investors know he’s not Nigerian. That changes what’s expected. The communication work of ensuring those expectations are calibrated to reality is on the founder.

The space ran in two linked sessions, and you can feel how much ground that covered. What stuck most, cutting across all four panellists: the market has reset, but it hasn’t closed. The founders who get funded are the ones who set targets, hit them, tell their investors the truth the whole time, and treat exits as something to plan for on day one, not something to figure out later.

Download the State of Startup Funding in Africa report.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: May 7, 2026