In this article, we exhume what predatory lending is, its examples and what can be done to curb it.

Lending and borrowing date back to the ancient Greeks and Romans. Pawnbrokers usually offered loans while collecting collateral from borrowers to reduce the risk of default. Collaterals ranged from the exchange of goods to even exchange for service.

In ancient Mesopotamia, farmers borrowed seeds with the promise of handing a portion of the harvest to the lender. To curtail default, the Laws in the code of Hammurabi provided that;

if anyone fail to meet a claim for debt, and sell himself, his wife, his son, and daughter for money or give them away to forced labor: they shall work for three years in the house of the man who bought them, or the proprietor, and in the fourth year they shall be set free.

In the present day, lending and borrowing remain at the crux of the world’s financial system. It is why banks are still in business, why some countries can finance their national budgets and why your bank sends you fifty naira at the end of every month and tags it as interest income.

However, the ever-changing dynamics of human financial needs, the need for financial institutions to adjust to these changes, and the proliferation of digital lenders (thanks to the Fintech boom) have given rise to a form of lending, slightly different from what used to be the status quo.

Introducing unsecured personal loans

As the name implies, these loans are not backed by any form of collateral. The lender lends the borrower a certain sum of money without receiving any tangible form of guarantee (except we want to count a contractual agreement to pay on the due date as one).

To combat the high level of repayment risk inherent in transactions of this nature, lenders decide to place an above-market interest rate on these loans. However, the subjective definition of “above-market interest rate” leaves a vacuum that some lenders have rushed into, and this brings us to the nucleus of this conversation — Predatory Lending.

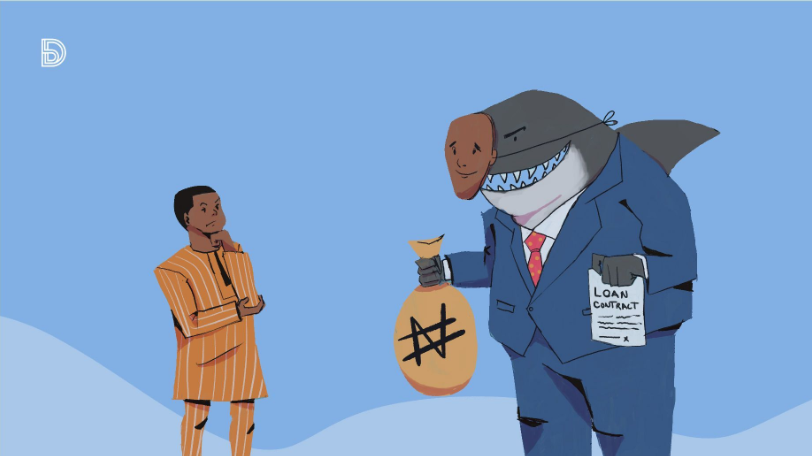

Predatory lending in Nigeria

Simply put, predatory lending is any form of lending that involves unethical lending practices seeking to enforce unfair and abusive loan terms on borrowers. Predatory lenders employ deceptive and aggressive sale tactics to attract unsuspecting borrowers into taking loans they cannot afford. Succinctly put, they are the metaphorical wolf in sheep’s clothing.

In 2020, the Covid-19 pandemic threw millions of people around the world into financial troubles. Jobs were lost, factories shut down, businesses closed their doors, and the entire world stayed indoors.

Nigerians were not excluded from this. The COVID-19 impact monitoring survey released by the Nigerian Bureau of Statistics reported that about 42% of Nigerians who were working before the outbreak of Covid-19 lost their jobs due to the impact of the pandemic. This financial uncertainty made individuals gravitate towards digital lenders, who at that time appeared to be the only source of financial help.

Most of these digital lenders offer loans as low as 5,000 naira and as high as 150,000 naira, depending on the borrower’s track record, with repayment periods usually capped at 30 days and interest rates ranging from 20% to 28% a month. The borrower is promised a gradual reduction in interest rates and an increase in credit limits in return for continuous patronage and timely repayment. Although the rates are almost never reduced, borrowers who have built their financial stability around these loan offerings keep going back, and the vicious cycle continues.

“They advertised that interest rates would be reduced and there would be an option to spread loan repayments. However, after starting with 10,000 naira and building my loan limit up to 100,000, there has not been a noticeable reduction in interest rates, and I still must meet up my loan obligations within one month,” says Lolade, a user of Fairmoney app.

Eleazar, who used loans from Kwikmoney to supplement his monthly Federal Government allowance while as a Youth Corp Member in 2018, says that the high rates were initially not an issue as it looked little compared to the loan amount. However, as he continued accessing loans, the interest charges began to turn into a financial burden.

“Initially, paying 700 naira on a loan of 5000 naira did not seem important. As I started increasing my loan limit, I realized that interest charges were quite substantial. But it was too late. My lifestyle was built on credit, and I had to remain in the toxic relationship even until after my first job.”

Data Privacy — A myth to digital lenders

Predatory lending does not end at excessive interest rates and hidden charges. Some digital lenders have taken it a notch higher by completely disregarding data privacy regulations.

In a joint report by Ikigai Innovation Initiative, Tech Hive Advisory, Reg Compass, and NaijaSecForce, it was revealed that some Digital lenders violate the data protection rights of their users. Some of these violations included excessive data collection, listening to user’s phone calls, reading SMS, installing trackers capable of profiling users, and sharing personal data with third parties without obtaining user consent.

House of Representative member, Honorable Akin Alabi recently took to Twitter to call out Lotus Credit, who he claimed had harassed him via a WhatsApp chat and threatened to list him as an accomplice if he does not contact the defaulter.

In recent times, regulators have begun to hold digital lenders with a stronger arm. Soko Loan, a popular digital lender, was fined the sum of Ten million Naira by The National Information Technology Development Agency for data invasion. This was on the back of a series of complaints against the company for unauthorized disclosures, failure to protect customers’ personal data, defamation of character, and carrying out the necessary due diligence as enshrined in the Nigeria Data Protection Regulation (NDPR).

Traditional banking institutions offer some respite

Recently, traditional banking institutions have forayed into the unsecured personal lending space. Banks like GTBank, Stanbic IBTC, and Access Bank currently offer instant personal loans at interest rates less than 2.5% per month.

“Commercial banks have really helped regarding offering access to cheap credit. I remember reaching out to my banker at a facility, and I was really wowed. Bro! it was cheap!” says Tayo, an auditor at a top audit firm in Nigeria.

However, the fact that these loan offers are only available to clients who have been able to meet some set criteria from the bank (e.g., Operated their bank accounts for a period as stipulated by the bank) leaves other individuals who are not that lucky at the mercy of digital lenders.

What’s it like from a lender’s perspective?

For Mejero Emmanuella, CEO of Pennee – a startup that provides small businesses with loans and management tools. The above-market interest rates are a reflection of the market. However, she feels that credit providers have the responsibility of full disclosure of interest rates to help borrowers make better decisions.

“The market is tough, capital is expensive – People are doing what they can to get a sustainable business. However, is there an alternative? Yes, it’s just more hard work and less virality. At the end of the day, I feel like credit providers should make their users fully aware of the interest rate they are paying so that they can make informed decisions” – Mejero Emmanuella, CEO at Pennee

On the question of risk management and the need to curb default, Emmanuella, whose company boasts of a sub 3% default rate, believes that lenders should be flexible in their approach as there is a thin line between being risk-averse and slowly morphing into a traditional bank.

She had this to say about risk management with lenders, “Risk management with loans is a continuous process. You cannot be 100% risk-averse, or else you become like the banks – providing loans for the seemingly overfunded. You have to give profiles the benefit of the doubt. It is personally important to me that the loans I provide can be paid back sustainably by the beneficiaries. So that involves some tests, here and there, before we scale what we have found to be true. That is also ridding ourselves of bias too and being swift to reconfigure risk lines when it is veering towards danger.”

Conclusion

The introduction of digital lending has provided a source of easily accessible credit to individuals whom the traditional financial system would have otherwise disenfranchised. However, the infiltration of digital lenders involved in predatory lending practices presents the need for the players in the space to actively curb the menace.

Government agencies like The National Information Technology Development Agency (NITDA) and The Federal Competition and Consumer Protection Commission should be actively involved in cases against lenders accused of predatory lending.

Also, the emergence of API Fintechs like Mono and Indicina has made it easier for digital lenders to access detailed financial information, which would help with determining interest rates, commensurate to the risk they would be undertaking and hence removes the need for arbitrary rates.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: December 19, 2024