The Central Bank of Nigeria (CBN) introduced the cashless policy to Nigerians in 2012. The policy aims to ensure that citizens embraced electronic transactions more than they did physical transactions.

The cashless policy enhanced the adoption of advanced electronic payment options. Asides from the regular over-the-counter transactions, the financial services industry rode on the policy to build infrastructures that facilitated swift and seamless payments. Infrastructures like; mobile banking, USSD, internet banking, and POS.

However, as the adoption of these advanced payment channels that boosted this policy grew, the country’s financial fraud rate peaked as well. These fraud attacks threatened the cashless policy and everything it represented.

The Nigeria Inter-Bank Settlement System Plc released a report on ‘Fraud in the Nigerian Financial Services’. The report covered the 2019 and 2020 financial year. Here are three takeaways from the report:

Coronavirus pandemic leads to surge in financial fraud

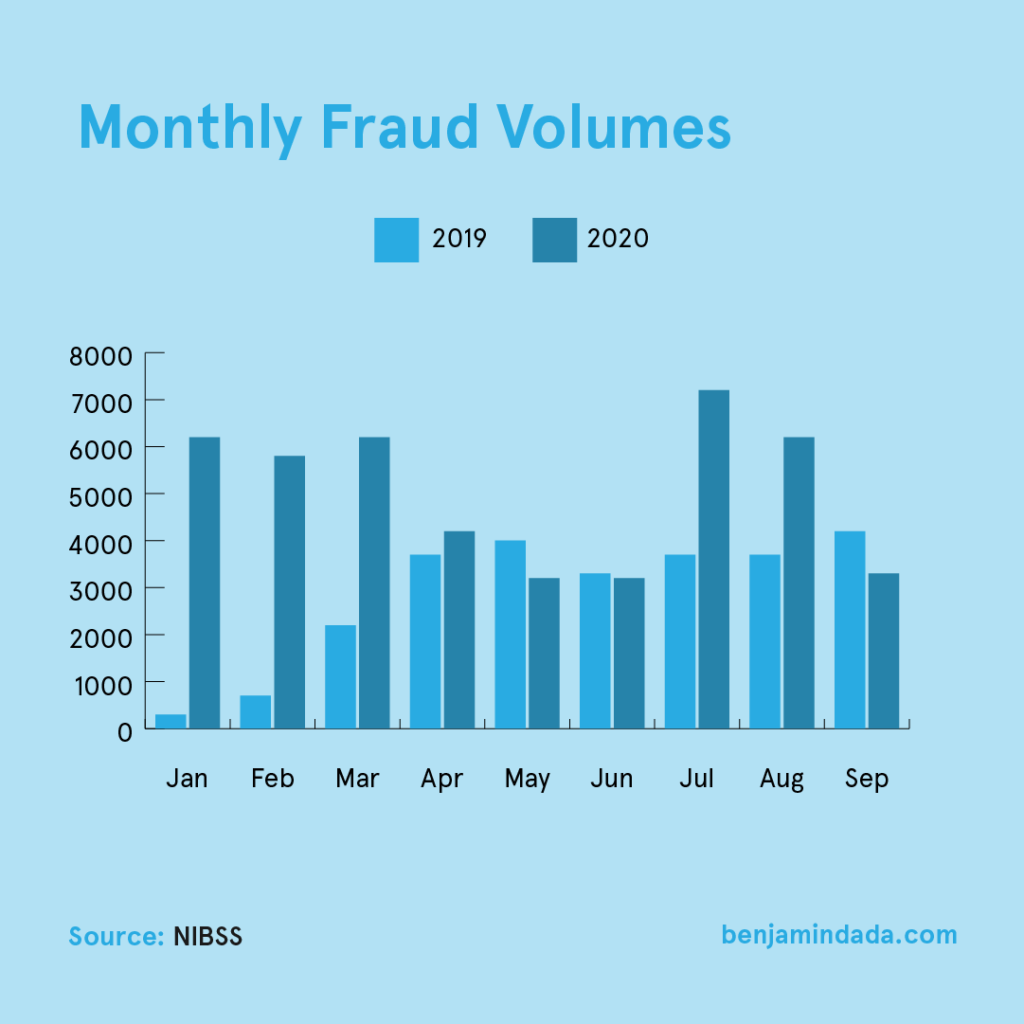

Financial fraud has been a recurring phenomenon in Nigeria. But 2020’s financial fraud was on a whole new level. The NIBSS reports that it peaked at its highest in 2020, accounting for a 186% increase against 2018 and, 2019 where its growth rate was low. The NIBSS blames the pandemic for the surge.

The COVID-19 lockdown began in March, causing people, businesses, and the government to embrace remote work and connections. It forced people to take their businesses and social connections online.

With the lockdown in place and everyone at home, people depended on technology to transact. This heavy traffic on the internet slowed down internet connectivity and caused delays in email and web filter updates. The NIBSS reports that these delays opened up an opportunity for e-scammers to spear-phish their targets.

By records, Nigerians are predominantly poor. The lockdown seemingly accelerated the hardship for Nigerians as it limited business activities. A Kaspersky 2021 insight elaborated the impact of the pandemic in Africa, recounting that it sparked both traditional and digital crime.

This spike in financial fraud can be blamed on so many things, ranging from loss of jobs, economic recession, inflation which stood at 12.88%, and loss of income. It is evident that the lockdown caused unrest and hardship which could have led citizens to perpetuate these crimes.

The report revealed that these scammers leveraged social engineering– a range of malicious activities accomplished through human interactions, to obtain sensitive data from their victims and carry out fraudulent transactions on their accounts.

Mobile records the highest growth YoY

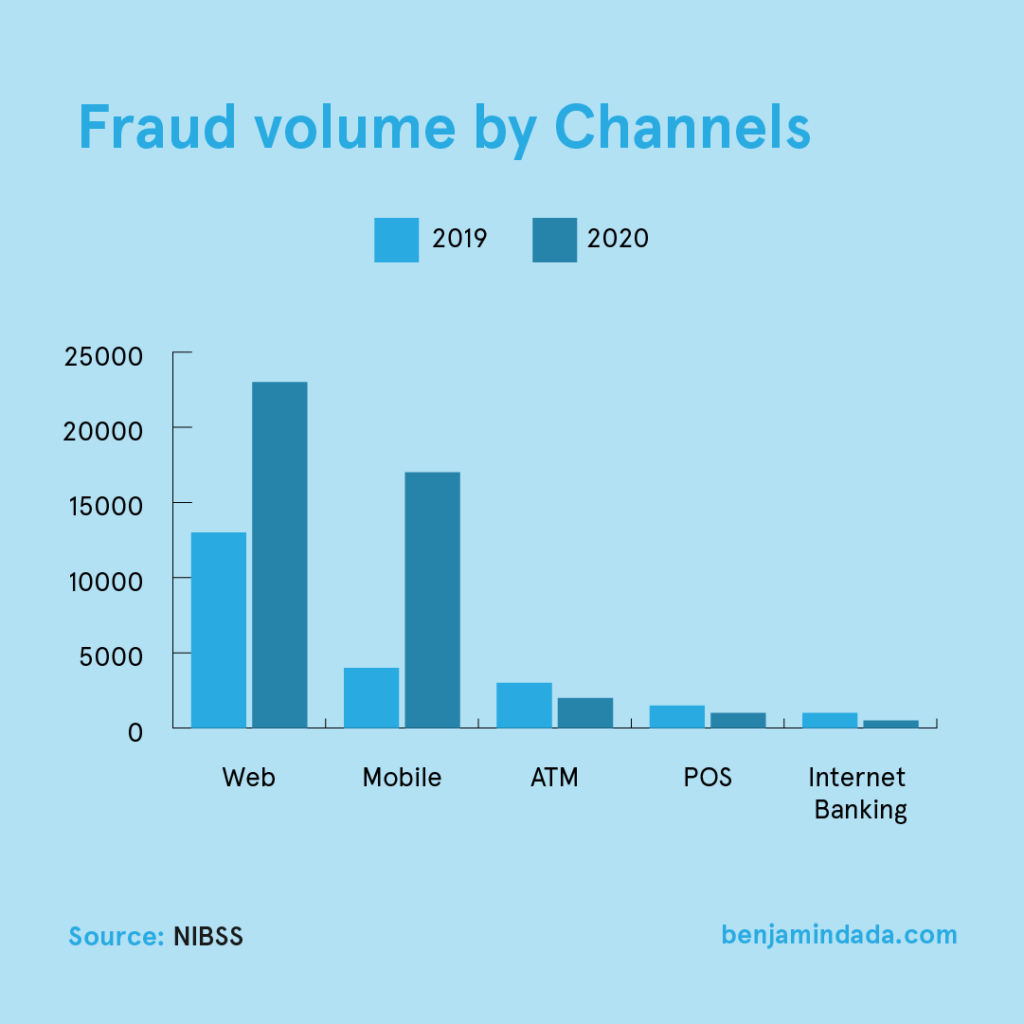

The COVID-19 pandemic accelerated the adoption of e-payments. According to another NIBSS report, mobile at 43% was the most preferred payment channel while USSD ranked closely at 35%. The report reveals that mobile devices were used to handle payment transactions 933.66 million times and USSD transactions 422.70 million times in 2020.

This means that mobile devices accounted for over 70% of transactions. This spike was achievable due to the mobile phone penetration rate in Nigeria. The country boasts of 97 million internet users and a 49.5% smartphone ownership rate.

Just as mobile led the way in payment transactions, it also recorded the highest growth in enhancing fraudulent transactions. The NIBSS recounts that mobile-led fraud channels saw a 330% Year-on-Year growth in 2020.

Although mobile-led channels recorded the highest growth, it wasn’t top of the list in enhancing financial fraud. The list was topped by web channels followed closely by mobile.

Mobile devices recorded the highest growth in enhancing fraud mostly because it was a tool of choice. Another factor for the growth may be because its largely affordable against a laptop device.

Financial Education is Key

To mitigate these risks, financial institutions need to put certain measures in place. The NIBSS recounts that data and customer education are the two major ways to fight financial fraud in Nigeria.

The financial services industry needs to sensitize its customers on how to identify and avoid interaction with these e-scammers. Customer detection is key to limiting fraud damage. All financial services providers must ensure that their customers are always at an alert regarding fraudulent activities.

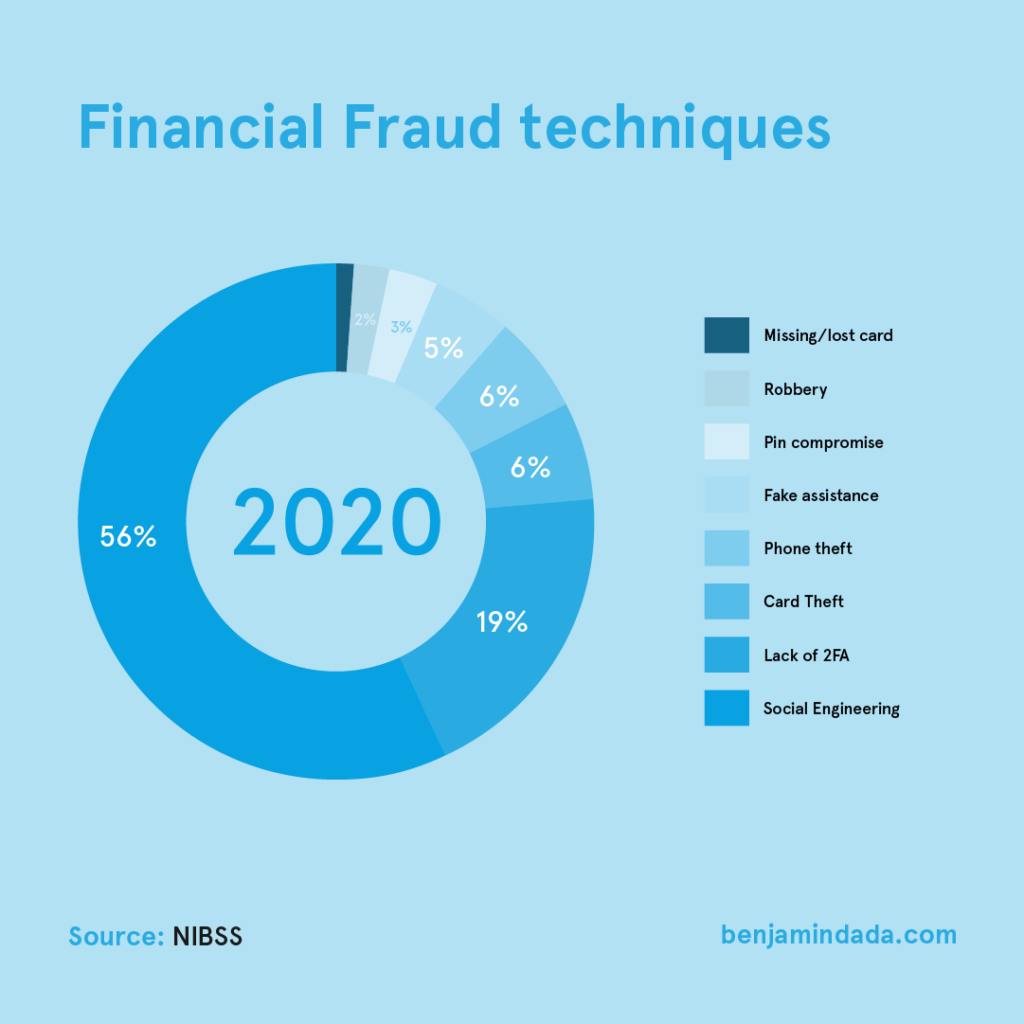

According to NIBSS, social engineering was the most common fraud technique in 2020. It accounted for 56% of all financial fraud. The lack of two-factor authentication (2FA) followed social engineering, accounting for 19%, card and phone theft each accounted for 6%. Next on the list is fake assistance which accounted for 5%, pin compromise accounted for 3%, robbery accounted for 2%, while missing/lost card accounted for 1%.

Fraud attacks through techniques like social engineering and two-factor authentication could have been easily avoided if customers were sensitized.

There is a need for financial institutions to leverage multiple communication channels like; emails and social media to constantly raise awareness of their fraud protection services. Asides from sensitizing their customers, financial institutions also need to be prompt in detecting and blocking any fraudulent activity that could affect their customers.

Data plays a huge role in accurate decision-making. The report further stated the need for in-depth research of the historical trends of fraudulent activities. Such research exposes the behavioral patterns of fraudsters and the characteristics of their victims.

The data gathered from the trends will also give the industry leverage to build effective solutions to the attacks. Should data analytics be attached to it, financial service providers can ride on the analytics to identify malicious activities and quickly nip it in the bud.

The industry needs to evolve with advanced anti-fraud innovations that will place them steps ahead of the scammers. These measures will positively impact and boost the confidence of the customer in their services.

The NIBSS opines that data risk assessments, policies, procedures, and controls births knowledge gaps that give way to financial fraud. In return, they advised that financial institutions invest in advanced anti-fraud solutions that will leverage AI (Artificial Intelligence) to provide top-notch protection against fraud.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: November 21, 2024