Between January and late March 2026, the Condia funding tracker recorded 59 deals spanning 14 African countries, with disclosed funding totalling approximately $705 million. The numbers reveal an ecosystem in the middle of a shift, with debt gaining ground on equity, growth-stage companies pulling in the largest rounds, and the same “Big Four” markets continuing to dominate.

Debt is no longer a last resort

The most striking signal in the Q1 2026 data is the rise of debt financing. Of the 59 deals tracked, 15 were pure debt rounds and 4 were a combination of equity and debt, meaning nearly a third of all deals in this period involved some form of debt instrument.

For much of Africa’s tech funding history, debt was something you turned to when equity dried up. The story in early 2026 looks different. Egypt’s ValU raised $63.6 million in debt from the National Bank of Egypt. South Africa’s SolarAfrica closed a $94 million project debt round from Rand Merchant Bank and Investec. Kenya’s Cold Solutions pulled in $19 million in debt from Mirova. These show structural choices by mature companies that have found a more cost-effective way to grow.

When you add the numbers up, pure equity raised roughly $212 million, while debt and hybrid instruments accounted for more than $490 million combined. Debt has overtaken equity in terms of capital volume in Q1 2026.

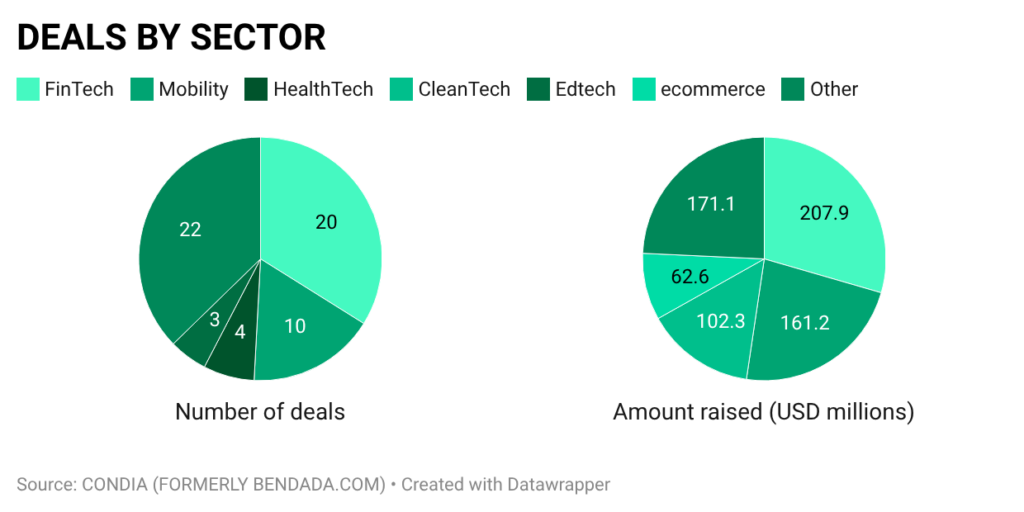

Fintech still leads, but the competition is high

Fintech recorded the most deals of any sector in the quarter, with 20 out of 59, and raised approximately $208 million in disclosed funding. That dominance is consistent with every prior year of African tech data.

Mobility startups raised around $161 million across 10 deals, powered by big rounds like GoCab’s $45 million in Côte d’Ivoire, Zeno’s $25 million in Kenya, and Max’s $24 million in Nigeria. CleanTech pulled in $102 million across just three deals, nearly all of it coming from SolarAfrica’s $94 million project round. AgriTech attracted $59.5 million, led by Sistema.bio’s $53 million growth round in Kenya.

The gap between fintech and everything else is narrowing, not because fintech is slowing down, but because energy, mobility, and agriculture are finally attracting the kind of capital that matches the size of the problems they are solving amidst the current geopolitical energy wars.

Growth-stage companies are winning the biggest cheques

Early-stage deals made up the bulk of the volume. There were 14 seed rounds, 5 pre-seed deals, and 6 Series A rounds, which shows an active base of new companies being built in the ecosystem, but the money is concentrated at the top.

Growth-stage companies raised roughly $271 million across 13 deals. That is more than any other stage, and nearly 40% of the total disclosed funding. The average growth-stage deal in this dataset was approximately $20 million.

SolarAfrica, ValU, Breadfast, GoCab, Spiro, and Max all raised growth-stage rounds above $20 million. These companies are not proving a concept. They are expanding infrastructure, entering new markets, or deepening their penetration in markets they already understand. Investors in early 2026 are still writing seed cheques, but the largest bets are going to companies that have already earned the right to ask for more.

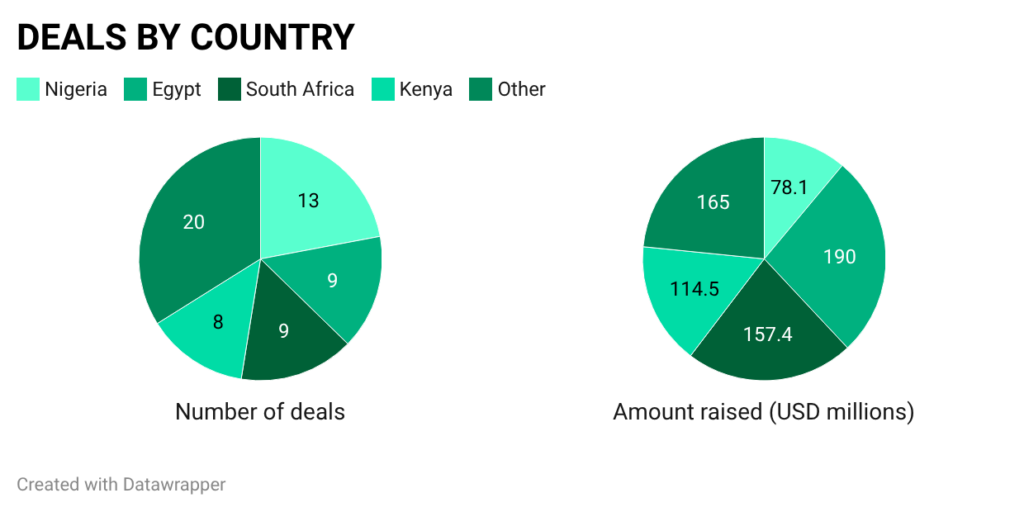

Nigeria leads in deals but not in capital.

Nigeria recorded the highest number of deals in Q1 2026, which reflects the country’s startup activity and the volume of early-stage companies being built there. But in total capital raised, Nigeria’s $78 million fell well behind Egypt’s $190 million and South Africa’s $157 million.

The reason being that Egypt produced two of the quarter’s five largest deals. ValU’s $63.6 million debt round and Breadfast’s $50 million pre-Series C alone account for more than $113 million.

Kenya came in third with $114.5 million across seven deals driven by logistics, mobility, agritech, and healthtech. Sistema.bio’s $53 million growth round and Zeno’s $25 million Series A were the anchors.

Morocco emerged as a quiet overachiever. Seven deals were recorded, but most were small, with a total of $23.4 million, spread across mobility, proptech, retail tech, and martech. The market is active, with companies like Yakeey ($15 million Series A), Enakl ($2.3 million seed), and WafR ($4 million seed) all closing rounds in the quarter.

South Africa’s $157 million came from a small number of large deals. SolarAfrica’s $94 million dominated, but Enko Education’s $22 million debt round, Lula’s $21 million, and smaller rounds from Orcafraud, NjiaPay, littlefish, and HappyPay rounded out a strong quarter for the country.

Pan-African companies raised $59.5 million, driven almost entirely by Spiro’s two rounds totalling $57 million for its electric motorcycle business.

The sectors that are coming up

Beyond the headline sectors, Deeptech had three deals but raised $36 million, two of them from Terra Industries in Nigeria. The company raised $11.75 million in January and then returned for another $22 million in February, both rounds within the same quarter.

AgriTech’s $59.5 million came from three deals across very different markets: Rasad Nigeria ($1.5 million debt from Sahel Capital), Lovegrass in Ethiopia ($5 million from British International Investment), and Sistema.bio in Kenya ($53 million growth). Three deals, three different approaches, three different countries.

AI as a standalone category is still small, with two deals, $3.9 million, but Ayadata in Ghana and Cybervergent in Nigeria both closed seed rounds in this period, signalling that investor interest in AI-native African companies is beginning to translate into actual capital.

February was the most active month

Of the three months covered, 25 deals closed in February, raising approximately $376 million more than January and March combined. January recorded 20 deals worth $222 million, while March, still incomplete at the time of the tracker’s last update, showed 10 deals worth approximately $107 million.

The concentration in February reflects the natural rhythm of deal-making. January often sees delayed announcements from late-2025 closings, and first-quarter activity tends to compress into the middle month as founders and investors come back fully from the holiday period.

To close, Africa’s startups raised more than $700 million across 59 deals in the first quarter of 2026, and the numbers show that debt is ascending, growth-stage companies are commanding the largest rounds, and the same concentration in a handful of markets that defined 2025 has carried over into the new year.

Data sourced from the Condia funding tracker, covering deals announced between January 1 and late March 2026.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: March 29, 2026