Africa’s startup ecosystem raised more capital in 2025 than it did the year before. After two years of contraction, that mattered. But the more revealing story wasn’t the rebound itself — it was how the money returned.

Africa’s 2025 funding story did not suddenly emerge at year’s end. By mid-year, the contours were already visible. When we tracked the continent’s biggest startup fundraises in December, one pattern stood out early: size no longer meant equity. Only 3 of the 10 largest raises in 2025 were pure venture rounds. The rest leaned on debt, securitisation, and project finance, concentrated in energy, mobility, and asset-heavy fintechs.

Briter’s full-year data now confirms that shift at scale. What looked like isolated financing structures in July and October was, in fact, a systemic reordering of how capital flowed into African tech. Debt crossed the billion-dollar mark. Cleantech absorbed the largest cheques. And markets once defined by venture volume began trading speed for durability.

In other words, the story Africa told through its biggest deals in 2025 was the same one Briter documents across the entire ecosystem: capital didn’t return to chase growth. It returned to back infrastructure.

Infrastructure takes the lead

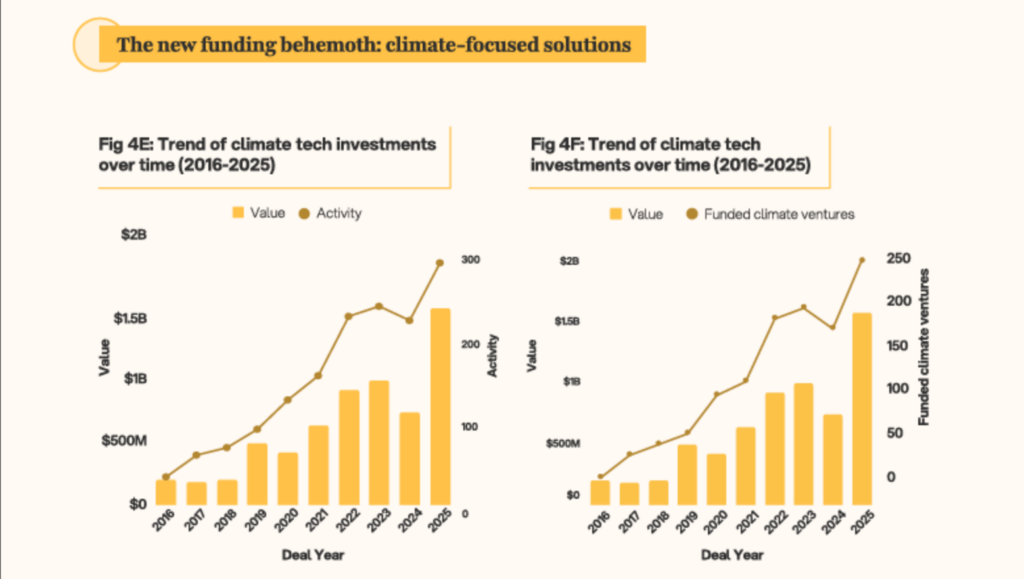

Energy and climate-focused companies pulled in roughly $1.2 billion, overtaking fintech to become the largest sector by total capital raised. Fintech still dominated deal count, but the biggest cheques flowed elsewhere—into solar generation, off-grid power, storage, and mobility systems that sit closer to the physical economy.

This wasn’t a sudden change so much as a recalibration. Investors increasingly favoured businesses with contracted revenues, asset backing, and long operating horizons over models tied to discretionary consumer spending. In a year marked by inflation, FX pressure, and tighter global liquidity, infrastructure offered something venture growth no longer did: predictability.

By mid-2025, the pattern was hard to miss. Many of the continent’s largest rounds resembled project finance more than classic venture capital, leaning on debt, securitisation, and blended instruments. Capital didn’t return to chase scale; it returned to back systems.

African tech, increasingly, is being valued as infrastructure: powering homes, moving goods, and stabilising economies long before it ships the next app.

Where the deals happened and where the money went

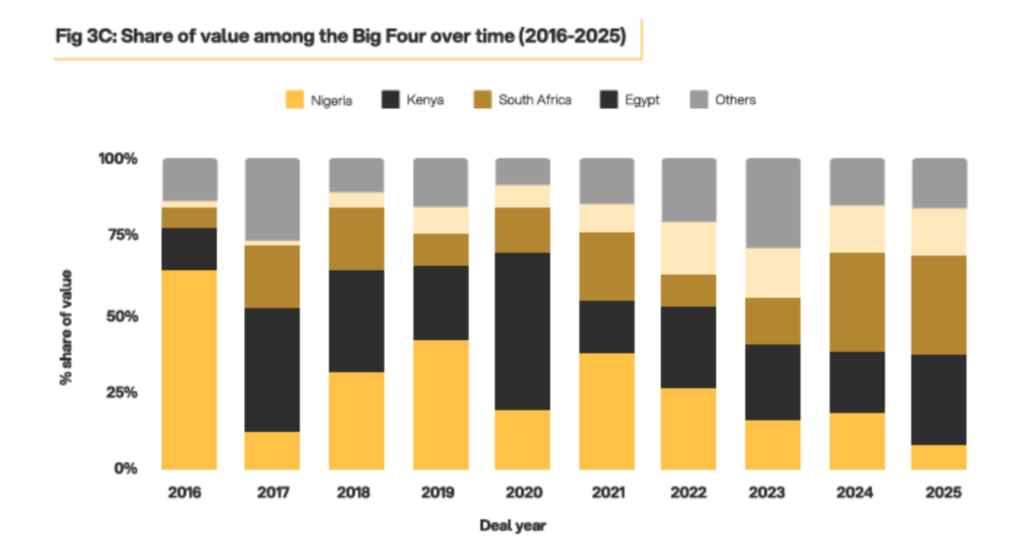

Nigeria remained Africa’s busiest startup market in 2025 by deal count, reflecting strong early-stage formation and steady seed activity. More companies raised capital there than anywhere else on the continent. But the biggest cheques increasingly landed elsewhere.

Capital spread outward. Kenya and South Africa captured a larger share of high-value rounds, driven by energy, mobility, and asset-heavy businesses that could absorb debt, project finance, and structured funding. Kenya, in particular, benefited from several outsized cleantech deals, while South Africa regained ground as the continent’s strongest equity market.

The shift signals a change in how investors read the map. Activity still matters, but scale now follows structure. Markets are being rewarded less for volume and more for their ability to support large, durable financings.

Debt enters the capital mix

One of the clearest signals from Africa’s 2025 funding landscape was the rise of debt financing. Over $1 billion was deployed into asset-backed companies in energy, mobility, and infrastructure-linked platforms, businesses with steady revenues and tangible collateral. For these founders, debt was an efficient way to grow without giving up control.

This points to a broader transition. More startups have moved beyond experimental growth into operational stability. They can service loans, structure facilities, and blend capital types. Equity is no longer the only route to scale.

The result is a more layered funding landscape. Venture capital concentrates on higher-risk models, while debt flows to companies that behave less like startups and more like infrastructure. Briter’s data suggests this is not a temporary adjustment, but a sign of a maturing ecosystem.

What “exit-ready” really meant in 2025

Exits resurfaced in African tech in 2025, quietly but clearly. Briter tracked 60+ acquisitions and secondary deals, ending a two-year liquidity freeze. Most weren’t splashy. They were trade sales: companies being bought for licenses, infrastructure, or cash-flowing operations, not growth stories.

The pattern followed the money. Fintech infrastructure, energy, logistics, and enterprise software found buyers. Consumer apps mostly didn’t. Outcomes clustered in Nigeria, Egypt, and South Africa, where acquirers already know how to do deals.

The signal is simple: exits came back selectively and only for businesses someone else could realistically run the next day.

What 2025 signalled

Entering 2026, African tech is operating with clearer constraints. Capital is harder, timelines are longer, and outcomes are more tightly defined. The ecosystem is still moving, just with less room for error.

What follows will be shaped by how well founders and investors work within that reality.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: January 27, 2026