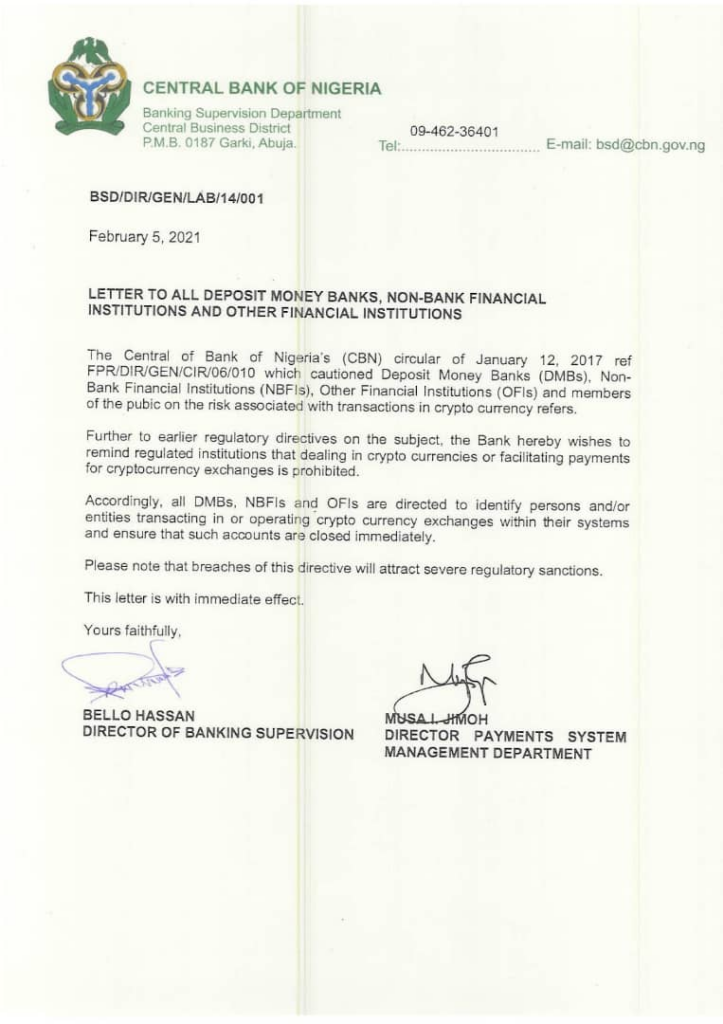

The Central Bank of Nigeria, today, announced a sweeping ban on cryptocurrency purchase and trading in the country.

The crypto ban was announced in a now-deleted circular dated February 5, 2021. The circular which bears the insignia of the CBN and signatures of two of its top officials, orders regulated financial institutions to identify people and organisations trading in crypto and close their accounts immediately. It threatens severe regulatory actions on financial institutions that refuse to co-operate.

The ban comes as a shock to many, including those in the crypto industry. Sources within the industry say there was no communication beforehand. While many expected some kind of regulation in the future, the suddenness and seeming totality of it has deeply shaken the industry.

The ban follows the path of recent regulatory practices where stakeholders are not consulted or even spoken to before restrictions are placed on their service. In December 2020, the SEC placed a ban on WealthTech company, Chaka. Industry sources say that Chaka only found out about the ban on the news.

It is also a reminder of the high-handed nature of the current administration as regards regulatory practices – no warnings no discussions, just punitive measures.

But crypto cannot be banned. How is the CBN doing it?

One of the most loudly touted advantages of bitcoin and other cryptocurrencies is that they are above regulation. That remains true.

However, what the CBN has done is to place restrictions on how people can buy and sell cryptocurrencies in Nigeria. The instructions in the circular prevent Deposit Money Banks (DMBs), Non-Bank Financial Institutions (NBFIs), and Other Financial Institutions (OFIs) from dealing in cryptocurrencies or even facilitating payments for crypto exchanges.

The CBN goes a step further to ask all regulated bodies under it to identify persons or entities transacting in crypto within their systems and close their accounts.

Most crypto exchanges partner with NBFIs and OFIs like Flutterwave, Paystack, and Monnify to transact with bank customers in Nigeria. The partnerships enable them to process debit card and direct transfer transactions. Based on the instructions in the circular, those companies cannot continue to provide those services.

In essence, the CBN is attempting to cut off the oxygen going to crypto platforms.

Think of it this way, the CBN neither produces gold nor does it control the availability of gold. However, it can stop banks and other financial institutions from allowing people within the system to buy gold. That’s what the CBN has done, but with crypto.

It follows that if people can’t buy and sell crypto, they can’t own crypto. Or can they?

Why is the CBN banning crypto?

Understanding why the CBN has banned transactions with crypto is key to undoing the ban, if it will ever be undone. In a fashion typical of the current administration, the CBN’s circular does not give any reasons for its ban.

The only hint is in the second paragraph where it says “…the Bank (CBN) wants to remind regulated institutions that dealing in cryptocurrencies or facilitating payments for crypto exchanges is prohibited”

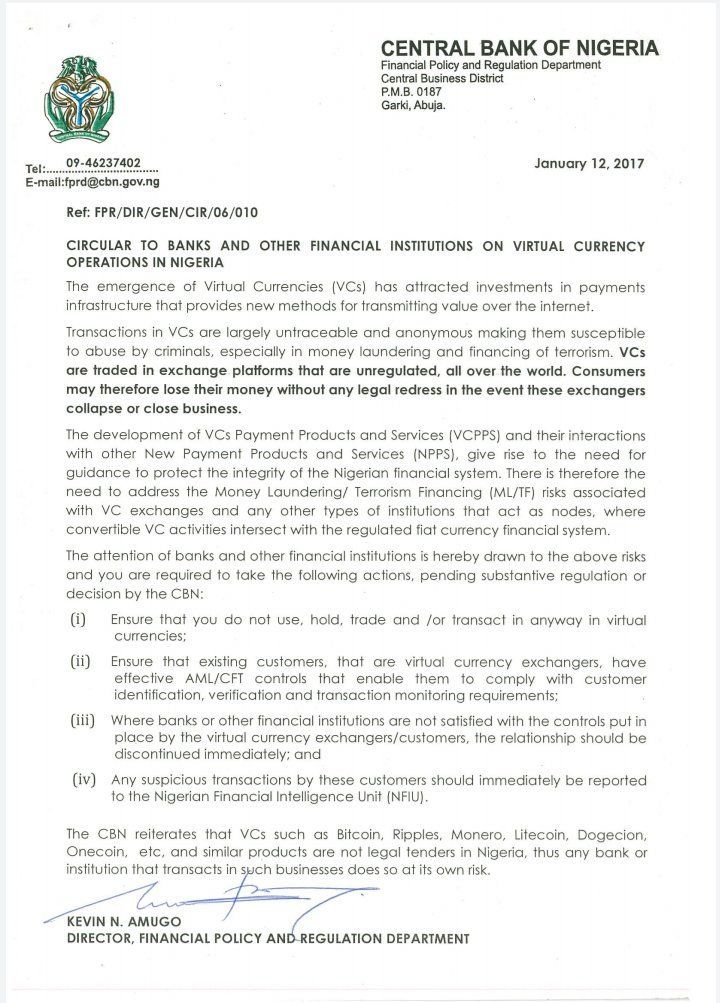

That sentence probably points to a January 2017 circular released by the CBN where it forbade regulated institutions from transacting in virtual currencies in any way. However, that was 2017 and this is 2021.

So, what has prompted the CBN to threaten sanctions on a policy it hasn’t enforced for the last four years?

While the CBN has not given any answers, a few educated guesses can be made. In the words of legendary rapper and music producer, Sean “P Diddy” Combs, “It’s all about the Benjamins”

Exchange rate control has been one of the core concerns of the current Presidency, and by extension, the incumbent CBN administration. While campaigning, the government made promises to return the naira-dollar exchange to “respectable” figures. However, since entering into power, the exchange rate has only fallen further, reaching prices of 480 NGN to 1 USD on the black market in late 2020. Now, the CBN faces an uphill struggle to stop the Naira’s free fall.

To achieve this, the CBN has implemented several remittance policies. While some have been hits, most have been misses. Some of the policies include restrictions on how much people can spend from their domiciliary accounts and how much can be spent on foreign transactions from naira accounts.

The combination of these policies and the lethargic state of the traditional banking system has brewed dissatisfaction among many Nigerians. This has led to many of them looking for alternatives for receiving foreign currency deposits.

Crypto companies have been working hard to solve the remittance challenge, albeit, without the cover and control of the CBN. In recent times they have become the go-to option for young Nigerians looking to receive foreign currency, especially from remote work.

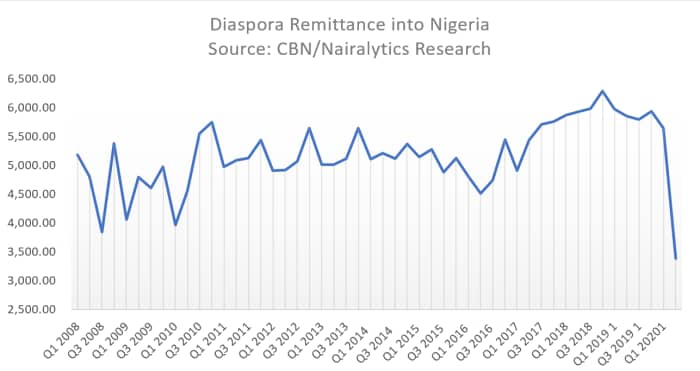

Pointers to the reason for the CBN’s new policy can be found by looking at the remittance figures for 2020. Between January 2020 and September 2020, remittances through official channels dropped from $2.05 billion to $54.4 million – a 97.3% fall.

The number one reason touted for the fall in remittances was the Covid-19 pandemic. Diaspora earnings were strained as a result of the pandemic and by extension, remittances suffered.

Other people suggested that the reason for the drop was that people were adopting other more efficient alternatives to send more – Cryptocurrencies. While the real reason for the drop has not been discovered, it was likely a mix of both factors.

In January, several crypto-companies active in Nigeria announced their transaction volumes for 2020. Here are some of the interesting numbers from 2020:

- Of the three which we have access to their 2020 numbers – Bushahub, Buycoins, and Bitsika-, the total transaction volume was just above $400 million.

- Bundle announced that it recorded $23 million in November 2020 alone.

- Quidax was said to be averaging around $778,000 per day in November too.

When other local players like Yellowcard, FrostPay, Instantcoins, Patricia, and RedimIT are accounted for, the total transaction volume for 2020 is likely to be above $1.5 billion.

Since a significant part of crypto transactions are remittances, it was always going to be a source of concern to a central bank that sees remittance control as a way to achieve its exchange rate targets.

Another speculative reason for the ban is the use of crypto during the #EndSARS protest. During the anti-police brutality protests that rocked the country in October 2020, young people resorted to crypto as a way to evade CBN restrictions on their accounts. It’s possible that the act of defiance also informed the decision.

What is the impact of the crypto ban on Nigerians?

Although it remains to be seen whether the ban on crypto transactions will be enforced, there is palpable tension in the air. If implemented it will prevent Nigerians from being able to fund and withdraw from their accounts in crypto exchanges.

While it does not criminalise ownership of crypto, the new circular makes owning and trading it more difficult for everyday people. In a time when many countries are exploring ways to make cryptocurrencies mainstream, Nigeria’s central bank has effectively taken the country back by more than a few steps.

Read: Bitcoin and the future of money in Nigeria

Questions have also been raised over the impact of the CBN’s latest move on the perception of cryptocurrencies by the general public. There are also concerns on how it will affect the relationship between law enforcement and owners of crypto. Law enforcement officials have been known to be high-handed, and sometimes, show misunderstandings of certain legal distinctions. With the new circular, the line is even blurrier for the uninformed.

The local crypto industry, which is also one of the most developed in Africa, will also face serious scrutiny going forward. After a largely successful year in 2020, local crypto startups were expected to spread their wings and fly. Potential fundraises and acquisitions were even discussed at the beginning of the year. Those plans will be put on hold now as the startups battle the uncertainty of the new regulation.

What is the way forward for cryptocurrencies in Nigeria?

It is important to note that the CBN’s notice is not a direct ban on cryptocurrency. The country’s apex financial body does not have the power to ban or criminalise crypto any more than it can criminalise the dollar, euro, or cedi. Rather, what it seeks to do is ensure that organisations regulated by the CBN no longer facilitate or participate in cryptocurrency transactions.

The way forward for cryptocurrency in Nigeria appears to be Peer-o-peer (P2P) transactions for now. Since ownership is not criminalised, everyday Nigerians can still own crypto and trade it among themselves without any hitches – provided financial institutions do not know what they are paying for.

The P2P market has always existed and is a bigger fraction of the crypto market than centralised exchanges and other crypto companies. The decentralised nature of crypto ownership and trading means people can still buy and sell among themselves.

According to an industry source, the only way the CBN could have achieved some kind of regulation was through centralised exchanges — which it has not cut off. While that is looking increasingly unlikely, it is an option that might still be explored. After all, the Nigerian government have been known to hit with highhanded sanctions and later soft pedal after meeting with stakeholders.

The re-emergence of P2P transactions means there will be more cases of fraud in crypto. Crypto startups will likely pivot to fill this need by providing P2P platforms where verified users can sell to one another.

Read: How to make money from cryptocurrency without getting scammed

A likely scenario is one where User A holds their cryptocurrency in an escrow with the exchange while User B transfers a sum of money equivalent to the crypto being purchased to the bank account of User A. On receipt of the naira equivalent, User A confirms the transaction and the crypto is released to User B.

P2P platforms like this are already popular all over the world with companies like Paxful and Remitano leading the way. In Nigeria, Buycoins also has a P2P offering.

Conclusion

All is not finished for Nigerian crypto startups. For many of them, this was a day they had anticipated and planned for. Although there are options to be explored, none of them are easy. However, if there’s anything you quickly learn as a Nigerian founder, it is that there are no easy ways to build.

Regulations are a necessary counterpoint for the eager arms of innovation. In this case, crypto startups are having to fight to make sure the arm is not cut off entirely.

Early communications from crypto startups have sued for calm with customers. The companies have also indicated that they are in communications with regulators to see how the issue can be resolved.

Hey Quidaxians,

We have seen CBN’s new policy but don’t worry your funds are safe and trading continues as usual.

However, all Naira deposits have been temporarily paused as CBN’s policy affects our payments partners.

Thank you for your support.— Quidax (@QuidaxAfrica) February 5, 2021

Thanks to everyone who has reached out. We are fully aware of the newest CBN circular and are going to be working with regulators to ensure our services are compliant. All trading on our platforms continues as usual, and all user funds are safe.

— BuyCoins (@buycoins_africa) February 5, 2021

It goes without saying that the crypto industry has taken a few step backs via this announcement. It will be a long road to recovery and full acceptance by the government. However, these companies have shown time and time again that they are willing to create solutions out of little. All bets are on the crypto companies to make it work eventually.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: November 20, 2024