In Nigeria, lending to informal workers has long been treated as a high-risk experiment. Banks demand documentation most traders cannot provide. Digital lenders step in, grow quickly, and then collide with defaults and public backlash.

Into that terrain, M-KOPA has built a credit portfolio that now spans more than one million Nigerian customers. Its advantage is not lower pricing. It is the ability to suspend access to the very asset it finances.

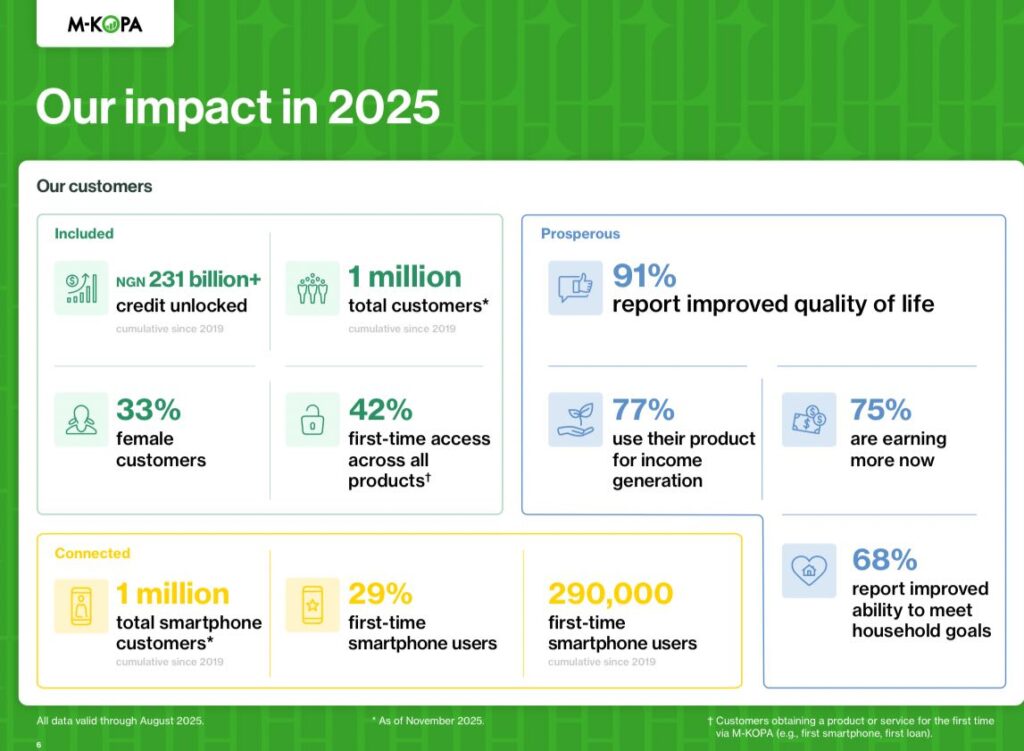

At the launch of its 2025 Nigeria Country Report in Lagos last week, the Kenyan-founded fintech confirmed it has crossed one million customers in the country since entering the market in 2019, making Nigeria its fastest-growing market globally.

The milestone is significant. The mechanics behind it are more revealing.

A cost-based model in a high-rate economy

At the launch event, Duroshola was deliberate about drawing that distinction. “We are not an interest-based model, we are a cost-based model.”

The point is practical rather than rhetorical. Nigeria’s benchmark rate now sits above 25%, and borrowing costs across the formal sector have moved with it. For households, that usually means repayments that adjust upward or loans whose true cost only becomes clear over time.

M-KOPA’s structure removes that moving target. The total repayment is fixed at the start and divided into daily instalments. Even if a six-month plan stretches beyond its original term, the amount owed does not grow.

For traders and gig workers earning in uneven daily cycles, that stability can matter as much as the price itself. Tomorrow’s obligation is the same as the one agreed on day one.

Enforcement without the courts

The more consequential innovation lies in enforcement. Each financed smartphone carries embedded software that ties usage directly to repayment. Customers make small daily payments aligned with their income cycles. If payments lapse, the device restricts functionality until the balance is cleared.

In practical terms, this replaces the traditional repossession process. In Nigeria, recovering physical collateral through courts can be costly and slow. By suspending access rather than seizing property, M-KOPA builds enforcement into the asset itself.

That design matters because the handset is rarely just a consumer gadget. The report indicates that 77% of customers use their smartphones or digital loans to generate income. For traders and gig workers, losing access to a phone interrupts supplier coordination, customer communication and digital payments. Default is not merely a missed instalment. It is a disruption to daily earnings.

During the briefing, Duroshola described Nigeria’s loss rates as single digit and said the country currently posts the strongest repayment performance across M-KOPA’s markets. In Nigeria’s unsecured lending segment, where default rates have frequently run into double digits, that performance suggests the structure of enforcement may be doing as much heavy lifting as the cost of credit itself.

From device financing to a credit ladder

The ₦230 billion deployed in Nigeria spans smartphone financing, cash loans and related products. Across more than one million customers, that implies average exposure in the low six-figure naira range per user—a level that only works if customers continue borrowing beyond the first device.

The relationship typically begins with the handset. Customers finance a phone over four or six months with daily instalments that mirror how they earn. As those payments come in, M-KOPA builds a repayment track record. That record becomes the basis for additional credit. Once consistency is established, customers can access cash loans, with the same device remaining inside the locking framework.

What starts as device financing turns into an ongoing credit relationship anchored in behavioural data. That matters in Nigeria, where the informal sector accounts for roughly 55% of GDP and employs most of the workforce. Many traders and gig workers have bank accounts and BVNs, yet lack the documented income trails commercial banks rely on to extend unsecured loans. They are economically active but often invisible to formal credit scoring systems.

By generating its own repayment history from the first instalment, M-KOPA creates a parallel credit file for customers who sit outside traditional underwriting models.

Scaling through informal underwriting

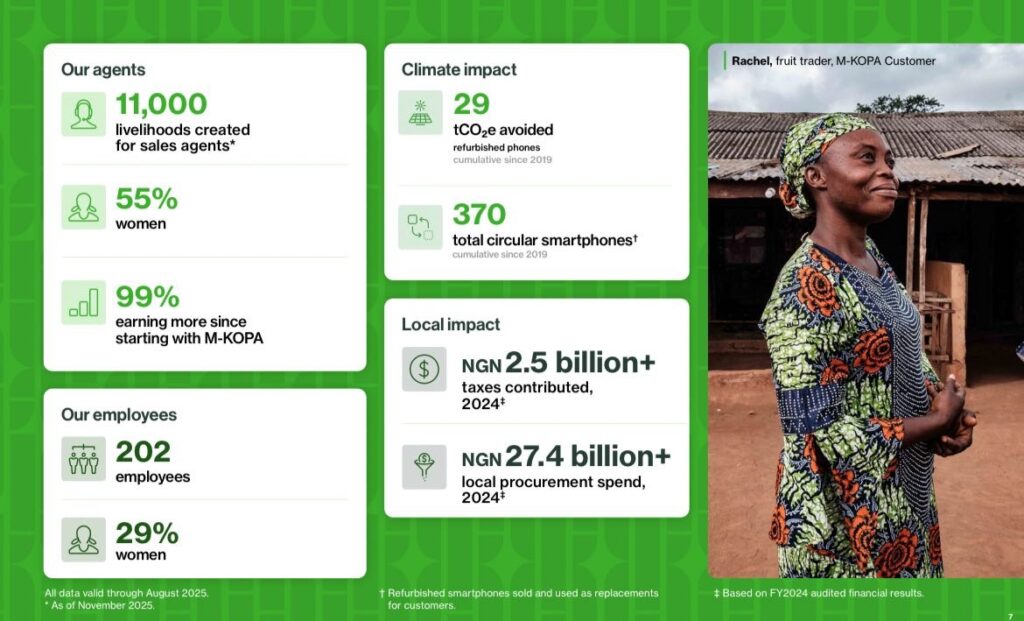

Unlike app-only lenders, M-KOPA’s Nigerian business is built on a physical network of 11,000 direct sales agents, more than half of them women. Agent churn stands at 0.1%. In a lending market known for short operating cycles and reputational volatility, that kind of stability is not incidental.

Agents onboard customers in person, walk them through repayment terms and remain present long after the initial sale. That physical layer does two things at once. It reduces misunderstanding at origination and embeds the credit relationship within communities where default carries social as well as financial consequences.

The structure also shapes how underwriting evolves. Repayment begins with a device tied to daily cash flow. Performance on that device determines access to additional credit. Each stage builds on observed behaviour rather than documentation.

As customers move from handset financing into cash loans, the mechanics remain familiar but the exposure changes. A device loan is straightforward to enforce because the asset and the credit are the same thing. Once cash is layered on top, enforcement still runs through the phone, yet repayment begins to rely more directly on the borrower’s income stability.

In that sense, the framework holds, but also stretches. The repayment discipline established during the device phase becomes the basis for larger credit. What will matter over time is whether the business income it supports remains steady enough to sustain additional borrowing.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: March 4, 2026