A new financial report has revealed that Gen Z is the most financially unexposed generation among adult Nigerians.

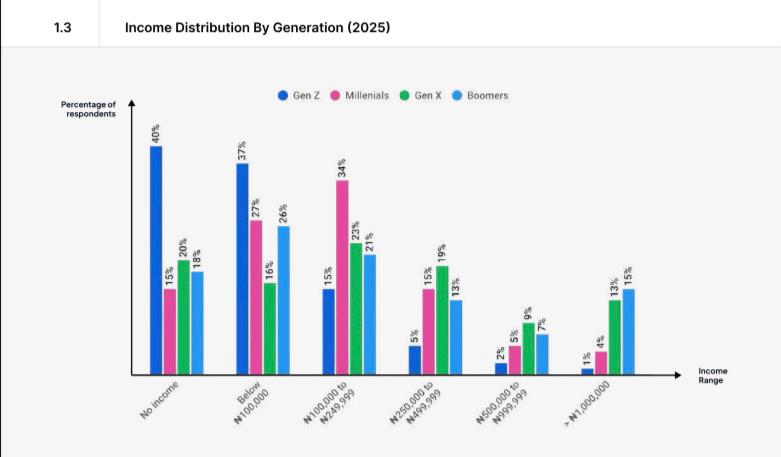

The report, titled Piggyvest Savings Report 2025 and released by the Nigerian fintech Piggyvest on Wednesday, shows that 40% of Gen Z (adults aged 18 to 28) have no monthly income at all. And of those who do earn something, 74% depend on a single income source, the highest rate of any generation surveyed. Millennials sit at 70%, Gen X at 63%, and Boomers at 60%.

In other words, Nigeria’s youngest adults are the most likely to have no income, the most dependent on a single source of money when they do earn, and the least protected when anything unexpected happens.

“Perhaps reflective of their early stage in the labour market and, for some, ongoing schooling or unstable employment, Gen Z Nigerians are the most likely to report having no income or earning below N100,000,” the report partly reads.

Piggyvest described the report, which followed a survey of 26,0000 Nigerians across all six geopolitical zones, as its “biggest and most comprehensive study yet”.

Why is this happening?

The National Bureau of Statistics has consistently shown that youth unemployment runs significantly higher than the national average. Many Gen Z Nigerians are still in school, recently graduated, or stuck in the informal economy doing gig work, petty trading, or task-based jobs with no salary structure and no benefits.

The minimum wage was raised to ₦70,000 in 2024, but as the report notes, inflation peaked above 33% that same year. The naira lost enormous purchasing power. So even young people who found formal employment entered the workforce with salaries that were already being eaten alive by the cost of food, transport, and rent before the month ended.

Add to this the structural reality that most Nigerian universities produce graduates faster than the economy creates jobs for them. A 2024 report estimated that Nigeria needs to create at least three million new jobs annually just to absorb new entrants into the labour market. It is not coming close to that.

The result is a generation where a huge proportion of young adults are technically in the workforce, hustling, trying, showing up, but are not earning in any formal or stable sense of the word.

No emergency funding

In practice, having no emergency savings means that if you fall sick, you either borrow money or you do not get treated. It means that if your phone breaks, you are stuck until someone helps you. It means that if your landlord gives you two weeks’ notice, there is no fund to draw on. Every shock becomes a crisis, and then it becomes debt or dependence.

“An emergency fund is what stands between a person and financial ruin when the unexpected happens, “ said Odun Eweniyi, COO of Piggyvest

A Vanguard study cited in the report found that individuals with even modest emergency savings report significantly higher financial well-being scores and lower stress levels, even after controlling for income and debt. The buffer is psychologically defining the difference between a person who can think clearly about the future and one who is permanently in crisis mode.

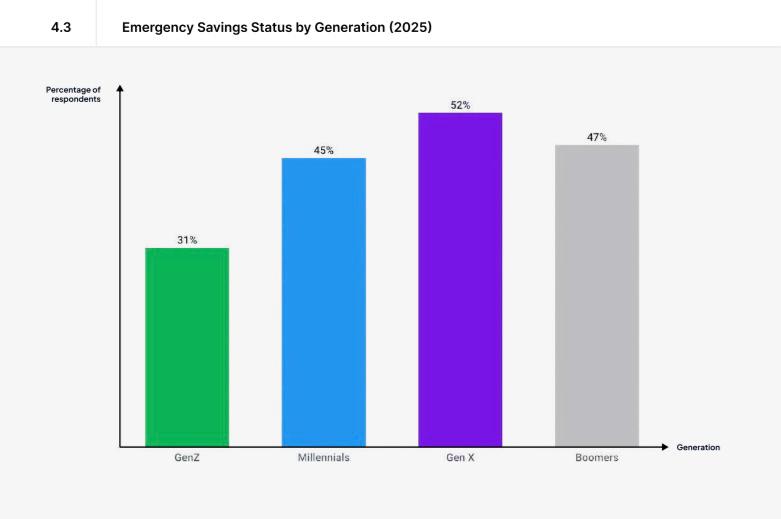

69% of Gen Z Nigerians do not have this buffer.

The Piggyvest report also shows that women edge slightly ahead of men in income diversification, with higher rates of multiple income streams. But broadly barriers remain as 60% of all female Gen Z respondents earn below ₦100,000 or report no income, compared to 56% of men.

It would be easy to frame this as a failure of individual discipline, about young people not saving enough and spending on the wrong things. The report pushes back on this framing. “Nigeria does not have a savings problem. It has a systems problem. The intent to save exists. The structures that make saving possible largely do not”. Eweniyi says

She claims that what needs to change is financial literacy embedded in the national school curriculum, tax-free savings thresholds for low-income earners, lower transaction costs, and macroeconomic stability that gives people a reason to save rather than spend their money before inflation erodes it further.

These are policy-level interventions that require government action, not just fintech innovation. And they are urgently needed, because the generation that is currently most financially vulnerable is also the largest demographic bloc in the country. Nigeria has one of the youngest populations in the world. A generation that cannot build financial buffers, cannot diversify income, and is simultaneously carrying family obligations will eventually produce consequences that the entire economy feels.

What can help Gen Z build stability

The report suggests that consistent saving habits are the strongest predictor of perceived financial stability, stronger even than income level. Among the small group of Nigerians who describe themselves as financially secure and content, 54% save a portion of their income every single month. Many of them are not high earners. What distinguishes them is the habit, not the amount. This points to the value of automated, low-barrier savings tools.

Diversification matters too. The data shows clearly that older Nigerians with multiple income streams are more financially stable. Starting early compounds over time.

To close, the Piggyvest Savings Report 2025 is, at its core, a document about adaptation. Nigerians across all generations are navigating economic pressure with resilience, but it has limits. Those limits are being tested earlier, harder, and with fewer resources than any other generation currently alive in Nigeria for Gen Z.

The 24-year-old sending money home while sitting on an empty savings account is not making bad decisions. They are making the only decisions available to him inside a system that has not been built to support him.

Until that system changes, the data will keep telling the same story.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: March 25, 2026