When Wasoko, one of Kenya’s most celebrated agtech companies, merged with Egypt’s MaxAB last year, the combined entity picked Cairo as its permanent home. The move read, at the time, like a straightforward business decision about market size. The data inside Briter’s State of Agtech Investment in Africa 2025 report, produced with funding from the Gates Foundation and the UK’s Foreign Commonwealth & Development Office, suggests it was also a signal that the industry was only beginning to process.

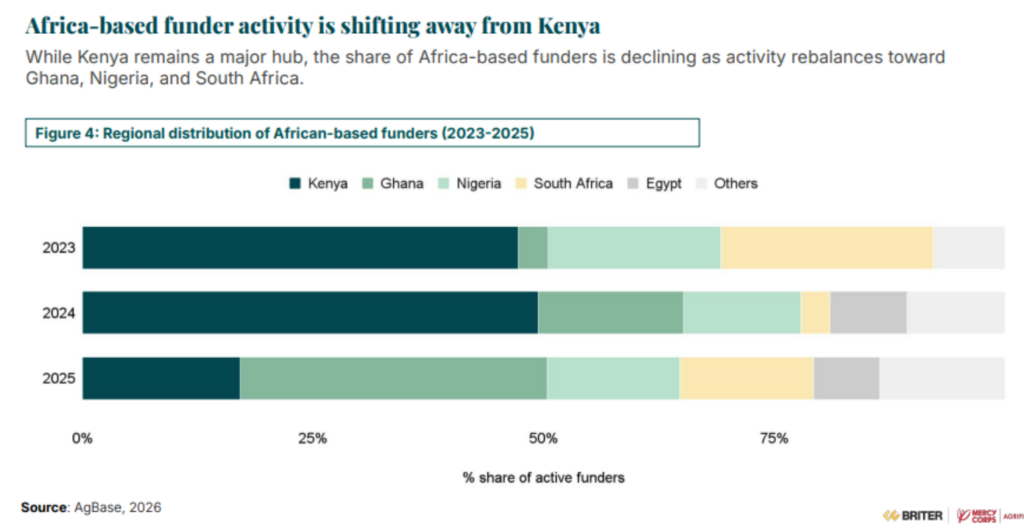

Kenya’s share of total agtech funding fell from over 50% in 2023-24 to roughly 25% in 2025, the steepest geographic drop the report records. That alone is striking. What sharpens it is where the movement is actually coming from. Between 2023 and 2025, Africa-based funders progressively shifted activity away from Kenya toward Nigeria, Ghana, and South Africa, and the report shows their share of activity in Kenya roughly halving over that period—which carries a different weight than foreign capital rotating out, given that these are the investors who have operated in these markets long enough to know exactly what they are moving away from.

The cost of being first

The report does not say Kenya is broken. What it shows is a market that has passed through its most venture-friendly phase. Mobile money penetration is high. The payments layer is largely solved. The digitisation plays that made early Kenyan agtech so attractive to impact-first investors have mostly been built, and their outcomes have been mixed enough to give the next wave of capital reason to pause.

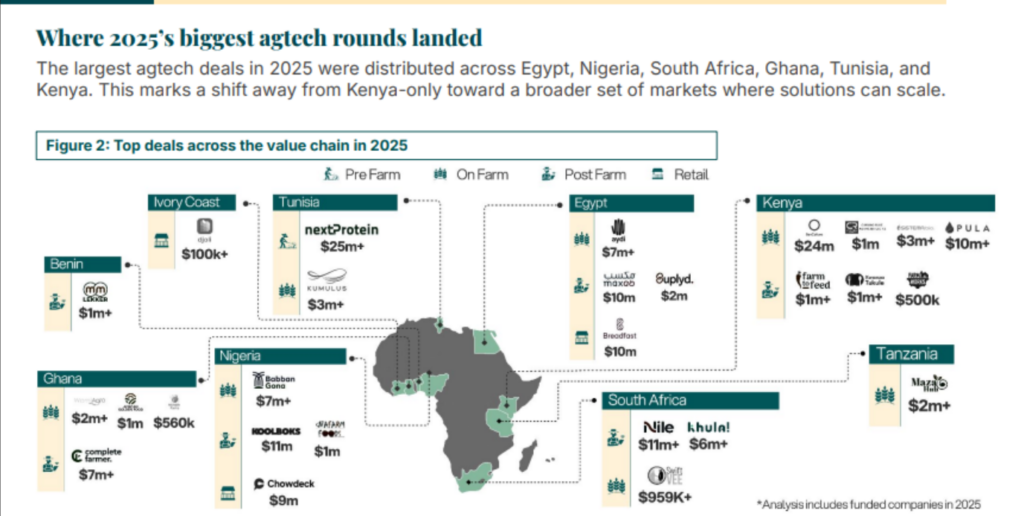

Of the 12 African agtech companies that crossed the $50 million funding threshold between 2016 and 2025, several are Kenyan-born, and several of those are no longer operating. Gro Intelligence shut down. Twiga Foods paused operations. Komaza closed. The report states plainly that high funding totals did not prove to be a reliable indicator of long-term sustainability, and the companies that survived were the ones that matched their capital structure to their actual economics rather than their growth narrative.

That is precisely where Kenya’s current structural problem lives.

The shilling against the dollar

Many of Kenya’s dominant agtech models: solar irrigation, asset financing, the hardware-heavy businesses that companies like SunCulture built, are capital-intensive by design, which means they depend on debt to scale. With domestic interest rates remaining elevated, much of that debt has been raised in US dollars. The mismatch this creates is not subtle. A company collecting shilling revenues from rural farmers in seasonal payments, while servicing dollar-denominated obligations, is exposed to currency movements in a way that doesn’t show up as a crisis until it already is one.

The shilling’s volatility in recent years has meant that what looks like a growth-stage business on paper can quietly become a debt-servicing operation in practice, with an increasing share of revenue going to lenders rather than to building anything.

This dynamic does not apply in the same way to Nigeria or Egypt, markets that are difficult in different ways but where the structural incentive to build infrastructure from scratch creates a different kind of leverage—and a different relationship with capital.

What Lagos is building instead

Nigeria is in a different phase, entirely fragmented, under-digitised, and where the model the report calls “winner-does-all” is taking hold. ThriveAgric, which has raised over $68 million, is the clearest example: rather than digitising access to credit or inputs, it bundles both alongside logistics and market access into a single integrated offering, building the infrastructure around the farmer rather than a service for them. The goal is to be unavoidable.

The capital structure reflects the shift. In 2025, equity accounted for less than half of total African agtech funding for the first time on record, with debt, hybrid instruments and grants making up the majority. That mix rewards businesses with hard assets and predictable cash flows, not impact-oriented on-farm platforms. What scales in that environment is infrastructure, and the infrastructure is being built elsewhere.

Kenya’s agtech ecosystem spent a decade establishing that the continent’s agriculture sector could be digitised and financed. The decade after will be defined by a different question: not how to reach the farmer, but who owns what surrounds them. That conversation is happening in Lagos and Cairo, and Nairobi is not leading it.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: March 18, 2026