Moniepoint to issue its own sterling (GBP) accounts to MonieWorld users, following the acquisition of an e-money issuer (EMI).

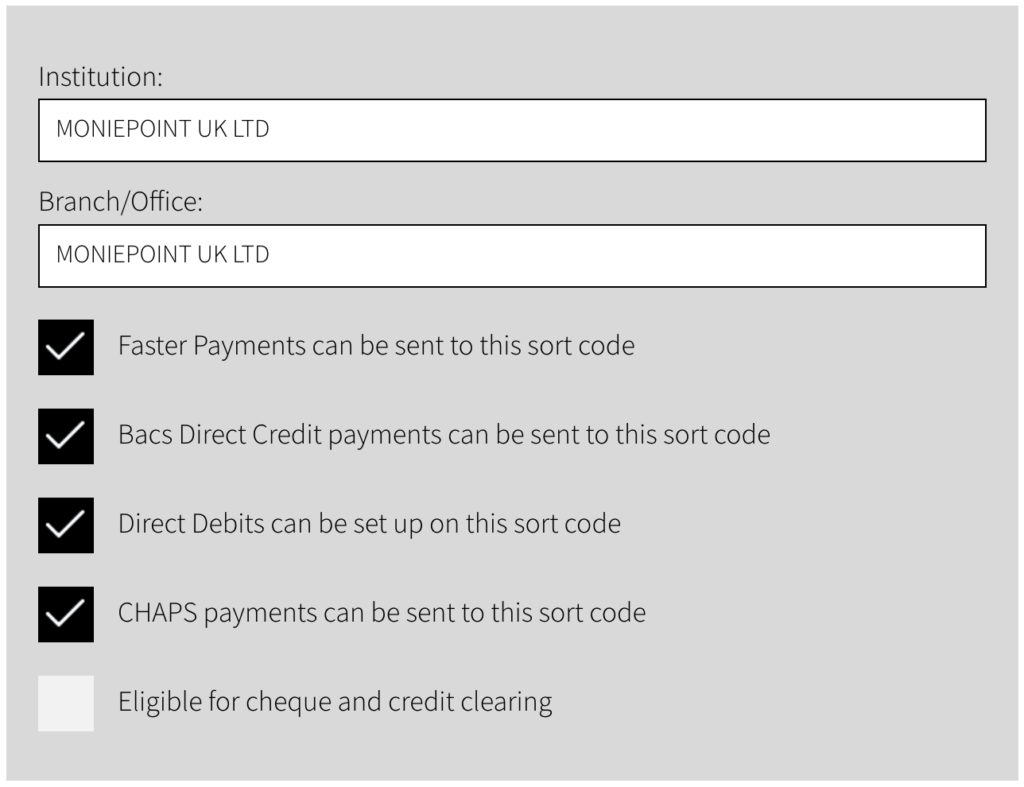

A subsidiary of Moniepoint Inc. (“Moniepoint”), Moniepoint UK Ltd will issue GBP accounts using its sort code 04-19-29. The sort code is connected to the major payment rails in the UK and can process Faster Payments (FPS), Direct Debits, Direct Credit (Bacs) and CHAPS. FPS is the instant payment system in the UK that allows residents to pay in or fund their accounts, and pay out or transfer money instantly.

This is a departure from the services provided by Moniepoint GB Ltd, which leveraged the e-money licence of PayrNet Limited (Railsr). “All new customer accounts opened on or after 1 December 2025 will be provided by Moniepoint UK Limited, and all customer accounts opened before this date will be migrated from Moniepoint GB Limited to Moniepoint UK Limited. You will be contacted individually to inform you of your migration date,” the company said on its website.

Indeed, in a customer email dated October 8, 2025, MonieWorld said, “From December 7th, 2025, your MonieWorld GBP account will be provided by Moniepoint UK Limited (“Moniepoint UK”) rather than by Moniepoint GB Limited (which is a distributor of PayrNet Limited [“Railsr”]).”

Why Moniepoint is switching from distributor to EMI

Moniepoint Group finally launched MonieWorld in April 2025. At launch, MonieWorld allowed UK residents to onboard and send money to Nigeria. Users can also create, fund, and hold sterling (GBP) on the MonieWorld app.

To launch such remittance business, a company would need a licence in the originating and receiving countries, alongside the financial partnerships and integrations that actually move money.

For its originating country licence, it opted for a partnership with an e-money issuer as distributor. While that potentially saved it six months (April – September), it placed their fate in the hands of another, the EMI they relied on, which is not acceptable for a company of their size and stature.

“As an agent or distributor, their branding, marketing, communications, risk appetite is all subject to the oversight of an EMI, who is in turn subject to their banking partner and other stakeholders’ choices and risk appetite, which can, of course, mean a change or interruption of service that has knock on effects for the agent/distributor,” says Alison Donnelly, Director, fscom, a leading UK regulatory consulting firm.

Owning a licence allows holders to be in more control of their destiny, “at least, to a great extent”, Donnelly adds.

A UK EMI licence grants holders, like Moniepoint, the ability to issue payment accounts, remit funds, connect directly to the instant payment systems, like Faster Payment (FPS), and even become members of Card schemes, like VISA and Mastercard.

For access to the underlying EMI licence, existing technical integrations and EU passporting rights, Moniepoint acquired Bancom Europe LTD. On September 12, 2025, it changed the company’s name to Moniepoint UK LTD.

In the future, one can expect Moniepoint to leverage these capabilities by issuing payment cards to its MonieWorld customers and launching in Europe.

Get passive updates on African tech & startups

View and choose the stories to interact with on our WhatsApp Channel

ExploreLast updated: December 10, 2025